Who is Truly Misinforming? Part 3

a FAQs Report sent by the Office of Speaker pro tempore Chuck Clemons. And my commentary. Seriously though How long can the City of Gainesville keep pretending?

Today I am continuing the commentary to the FAQs report put out by the Office of Speaker Pro Tempore Chuck Clemons. First, let me tell you Bryan Eastman will be talked about A lot in the rest of this. Many know that I speak my mind to the man, they know that I will call him out, and then I will also ask questions. Lately his denial has gotten out of hand, he has chosen to blame a state that is looking out for its people. In his own words “…It is just that the State of Florida has decided that they are going to beat up on Gainesville for a bit”, this tells me that he will not accept that the city has been at fault for this whole thing, and truthfully they will not be cutting back.

9) But don’t the Municipal Bond Rating Agencies think that GRU is still a good investment?

In his substack diatribe ironically entitled “Correcting the Misinformation on GRU”, City Commissioner Bryan Eastman opines that any concern over the financial health of GRU are “lies, misdirection, and falsehoods”. Eastman points to the current bond ratings held by GRU from the three municipal bond rating agencies - Moody, Standards and Poor’s, and Fitch (Aa3, A, A+, respectively)

(https://www.gru.com/Portals/0/2022%20updates/210860_Rating_Agency_Methodology_2022 0207.pdf, p.11)

Eastman begins this portion of his piece by stating outright – “I’m no utility financing expert...” and then sets out to prove that very point.

Eastman continues, declaring the bond rating agencies are oracles - “They don’t work for us, they’re neutral, and are ideal experts to show the actual financial sustainability of GRU.”

I like to believe that that statement is grounded in naivete and is ample evidence for an Authority comprised of professionals. There are reasons bond ratings agencies have a disclaimer longer than most novels.

Bond rating agencies are not neutral – they serve the interests of the investor whose only objective is understandably to make money. Further, a bond rating’s primary focus is not on the financial health of an entity, as Eastman rightfully points out in the article. A bond rating indicates the likelihood and ability for a borrower to repay the loan.

An entity can be in dire financial straits, however, the means to pay off the loan, no matter what it is, is the only thing rating agencies care about.

In the case of GRU, both Moody’s and Fitch identified those safety nets that have guarded against the total collapse of the utility’s bond ratings. Those safety nets are the monopoly enjoyed by GRU to provide an indispensable necessary service, coupled with an unencumbered means and little hesitancy to raise rates on customers in order to secure the requisite payments.

Moody’s applauds GRU’s “track record of raising rates as necessary.”

https://www.gru.com/Portals/0/2023%20Updates/Moodys-affirms-GRUs-FL-Aa3-09Feb2023- PR_908011739.pdf

Meanwhile, Fitch does concede that GRU is highly leveraged and heavily in debt, attributing elevated energy rates to GRU’s pursuit of higher fixed-cost renewable resources. However, Fitch notes:

“The electric utility has very strong rate flexibility reinforced by its legal ability to set rates. GRU’s rate-setting authority is subject only to City Commission approval,” and that “(GRU supplies) monopolistic utility services to a diverse and growing retail customer base, providing resilient and secure revenue sources for the system.”

In other words, “GRU’s customers are captive and they must pay whatever is demanded to underwrite the Commission’s next costly, non-revenue producing venture.”

Fitch also does an evaluation of how much blood is still left that can be squeezed out of the turnip. They note that the affordability ratio (the annual electric bill for the system and the median household income) still leaves plenty of room for GRU to raise rates.

https://www.gru.com/Portals/0/2022%20updates/Fitch%20Rating%20Action%20June%2023%2 02022.pdf

Eastman touts that GRU’s “ratings are higher than Florida Power & Light and Duke Energy.”

Certainly, they are, and they should be even higher. GRU’s bond rating is higher when compared with IOUs because while they are both granted a monopoly, only GRU can unilaterally set the utility rates they charge their customers. There is no excuse for a monopolistic entity that sets its own rates to provide a necessary good or service to a captive customer base to not have a AAA rating, yet here we are cheering on AA3’s, A+’s, and A’s.

Eastman lays claim to the assertion that the bond rating agencies “think GRU is doing fine!” But they don’t – otherwise they would not have downgraded GRU on 5 separate occasions in a 9-year period. This is a downward trajectory with no end in sight.

These downgrades are warning orders, with the bond rating agencies covering their behinds for having issued higher ratings in the past. Eastman conveniently leaves out the assessment by Standard and Poor’s which has downgraded GRU twice. S&P took GRU and its management to the woodshed stating, in part –

“The downgrade reflects GRU's very high rates and leverage, the product of investment in renewable resources that have proven to be uncompetitive. To maintain financial metrics and ensure full cost recovery, additional rate increases are expected over the next several years, which we believe will exacerbate GRU's already limited financial flexibility, presenting additional challenges is the recently adopted goal of reaching 100% renewable generation by 2045. In our view, there is heightened risk that achieving this goal will entail additional rate increases or debt. Furthermore, there is heightened risk of ratepayer backlash–which could turn what is now a vocal minority in opposition, into a vocal majority--with implications for financial metrics and strategic planning.”

In the midst of all that we know about GRU’s financial woes, pointing to our bonding ratings as an indicator that “all is well” is like hearing an addict protest, “I’m doing fine, just ask my drug dealer.”(Office of Speaker Pro Tempore Chuck Clemons)

Bryan Eastman, I feel continues to dig a hole deeper and deeper. He continues to repeat the same thing over and over. Proud to talk about such fabulous ratings by Fitch and Moody’s, but never says why the ratings are good. He has even referred to the rating reports, but I have to wonder if he thinks people just will not read the reports. These reports tend to say that the rating are because of GRU’s ability to raise rates. I do not know how many reports I have read that continue to say this. So, wouldn’t that mean that if GRU/The City of GNV did not raise the rates, the ratings would then be likely worse than FPL and Duke? I am fairly positive that would be the case. Honestly, why are they so worried about the ratings at this point when they see people with GRU bills higher than house payments? This shows a huge degree of narcissism on the part of the city. These commissioners are public servants, and they have shown they care more about a rating than those that voted for them. While Bryan Eastman continues to gaslight customers, and speak in circles like a dog chasing his tail, I do not think he has realized that many have caught on to his antics and are no longer blind to his political lies.

10) Is the contention false that the City of Gainesville has transferred more money than GRU has earned?

No, the City of Gainesville has annually transferred more money out of GRU than the utility has earned. Any review the utility’s financial statements using Generally Accepted Accounting Principles (GAAP) bears out this indisputable fact.

The real number of just how much money the City has transferred from GRU isn’t fully known as of yet. As noted in the Auditor General’s report, the City overcharges indirect costs to GRU by way of Service

Level Agreements (SLAs.) In the case of an SLA, both GRU and the City of Gainesville benefit from the expense of a good or service, but the City will charge GRU the brunt of whatever is the cost. (January 2022, City of Gainesville Operational Audit Report No. 2022-087, p. 1, Finding 3).

HB1645 dictates that the cost to GRU of such SLAs must be factored in when calculating the total monies that are annually transferred to the City; a practice that here-to-date had not been done.

Again, in Bryan Eastman’s substack article “Correcting the Misinformation on GRU”, he attempts to dismiss the claim that the Commission transfers more money to the City budget than the utility earns. However, Eastman goes one step further by decreeing that GRU is “in the black”. In the course of his trying to prove his assertion, again, Eastman displays why getting the Authority online quickly is so critical.

To prove his thesis that GRU is in the black, Eastman provides the following chart, culled from a Fitch deck, with the following caption:

“Fitch’s analysis of GRU’s operating margins. If we spent more than we took in these would all be negative, but they’re not. They show a healthy margin that allows us to pay our bond holders back and pay the GFT.”

Embarrassingly enough, what the above illustrates is GRU’s Operating Margin. An Operating Margin is merely the gross

profitability margin when deducting Operating Expenses from Operating Revenue – The total of payments received from customers for providing them a good or service minus the total of all direct cost to the business for providing that good or service.

It doesn’t include the subtraction of debt service and infrastructure capital, which is a necessary step in order to calculate an entities Net Earnings, or what everyone refers to as “profits”. In GRU’s case, the Debt Service is huge – it pays out close to $60 million a year just to keep the wolves at bay.

What the chart does prove is that, despite all the interference and mismanagement from the City Commission, the utility and its employees have the ingredients to build an exceptionally strong utility. It is the City Commission and their poor decisions that have pushed GRU into the precarious position it finds itself in today.

Eastman is bewildered where anyone could conjure the idea that the City of Gainesville was driving GRU further into debt, stating, “I have no idea where Rep. Clemons gets his numbers from, as they’ve never cited any public documents and it’s not in the JLAC report. It’s possible they’re using some Frankenstein accounting structure...”

Why no, it isn’t a Frankenstein accounting structure – it’s the GAAP; standard accounting that is clearly foreign to Eastman. We could spell out all the calculations which show how much of a deficit GRU has annually carried in order to satisfy the City’s transfer demands, however, because the financial statement has already done the calculations for us, there is a rather easy way to verify that number.

In the links below, scroll to the table entitled “Condensed Statements of Revenues, Expenses, and Changes in Net Position”

At the bottom of the table, note the entry “Change in Net Position”, if the number is in parentheses, that indicates a negative balance. (That figure alone should have had Eastman questioning just what the Fitch chart was telling him)

Take note of that number (remember if it is in parentheses, treat it like the negative that it is) and subtract it from the entry above it which indicates “Capitol Contributions net”. Capital contributions are considered performance neutral, since there is no profit or loss generated by the payment, and therefore it is not included in gross income for the purposes of calculating net earnings. As such, it is subtracted and the product is the net earnings of GRU for the particular year.

The following are the Net Earnings by year for GRU according to their audited financial statements. In 2022, +10,962k; 2021, (14,349k); 2020, (21,665k); 2019, (12,782k); 2018, (5,476k); 2017, (8,689k)

Discounting for a moment last year’s first recorded profit in some time, the total deficits which were a direct result of the City’s transfers in 2018, 2019, 2020, and 2021 amounted to $54,272k. While the number quoted in the past for the previous 4 years, was approx. $68,000k, it did not factor in the subsequent restatement of the 2018 operating revenue.

If you were to add the deficit from 2017, we find that over that 5 year period, the City transfers were $62,961k greater than GRU’s net earnings.

Even if when we add GRU’s 2022 positive earnings report, despite anyone’s claims to the contrary, over the last 6 years (2017-2022) the City of Gainesville has transferred a total of $51,999k more from GRU than the utility’s net earnings. (Office of Speaker Pro Tempore Chuck Clemons)

Really, I do not have much commentary for this, as We already know that I feel that Eastman is a dog chasing his tail. This part has a lot of great information that Eastman could benefit from obviously, his accounting classes taught him nothing.

11) But isn’t the percentage of GRU’s revenues transferred to the City of Gainesville low when compared with other municipalities who own utilities?

Again, another fuzzy math calculation courtesy of Bryan Eastman in his substack article “Correcting the Misinformation on GRU”.

In that article, Eastman states:

“The truth is that the General Funds Transfer is a revenue stream every utility uses, and the City of Gainesville’s is low compared to other utilities. Our transfer is 9.6% of revenue from the utility, making it significantly lower than Tallahassee (16.8%), Orlando (14.07%), Lakeland (13.25%) and others.”

He even provides this chart to further drive home his point –

Yet again, Eastman is either confused or disingenuous. He uses the utility revenues and not net earnings to manufacture a self-fulfilling prophecy. Utility revenues are the total of everything the business has made before a single dollar has been paid to its creditors.

An owner of any business should be the last to the pay window, but Eastman wants to focus on the revenue earned through the hard work of the system’s employees and not the number that includes the cost of a decades-long line of the City’s follies and mismanagement. All of those other MOUs in the chart have nowhere near the leverage, the number of non-revenue-generating assets, nor the exorbitant Debt-To-Net-Position Ratio of GRU.

If one were to make a bar graph with the percentage of net earnings transferred to each city, the City of Gainesville’s bar would have to come with a note that says, “continued on next page” because

historically, it has taken over 100% of GRU’s net earnings. I doubt very seriously whether any of those other MOUs would want to be lumped together in the same chart absent it being noted how much more financially stable and affordable they are than GRU.

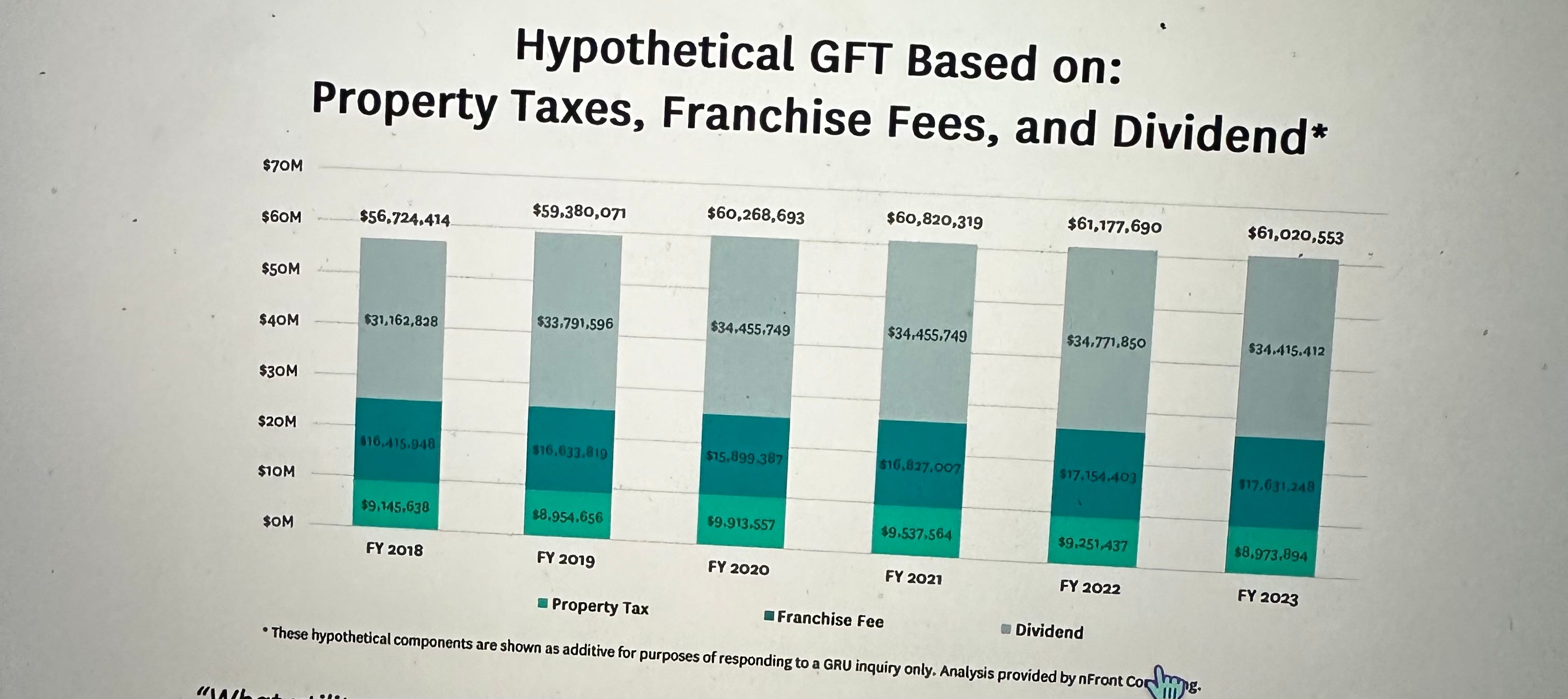

In his commentary underneath another chart on the same subject, Eastman laments that the amount of the annual transfer, doesn’t reach the levels that the City would charge an IOU by way of property taxes, franchise fees and dividends.

“What utility consultant nFront Consulting came out with that showed what GRU would be paying the city under a typical tax, franchise fee, and dividend scenario. The GFT has never been anywhere near this large”

“The GFT has never been anywhere near this large”, Eastman declares.

Perhaps he is correct, pending a review of the SLAs, but it is a tragedy that the net earnings of the utility have never been given the chance to grow and subsequently supplement the City’s budget to those levels. However, it has been the City Commission’s poor oversight and decisions, that were ridiculous in real-time, that have made certain that Wall Street gets fed before everyone else. (Office of Speaker Pro Tempore Chuck Clemons)

I could be wrong, but if Eastman claims that “the GFT has never been anywhere near this large” it have never been 61 million, but, it has been over 38 million evidenced here. The chart essentially tells me the property taxes and the franchise fees would make up the GFT, and like I said I could be wrong but looking at financial records and the graph somehow they will be playing shell games even more with your money. I mean how much more can the city of Gainesville screw up? With the last few meetings, I did not attend in person, but did watch from my home in my spare time, there really isn’t any cutting going on. It seems they are cutting from here to give it to another place. I couldn’t tell you how much I have realized that the small time politics seem to be a butt hair away from illegal corruption, if they haven’t already crossed that line. but I do believe that with the audit coming up, these shell games will be found out, and once again, I am saying I do believe there are going to be empty seats to fill. And maybe we will see if there really is anything illegal amuck.

Stay tuned for Part four which will be the final part to the series.